Multimodal AI Agents Are Coming for the Banking App. Here Is Why BFSI Should Pay Attention Now.

Multimodal AI agents handle voice, documents, and data in one call. Here is why BFSI institutions are replacing apps faster than expected.

A ground-level breakdown of how multimodal AI agents are displacing app-based interfaces for banking, insurance, and lending institutions.

What Is a Multimodal AI Agent? How Is It Different from a Chatbot?

A chatbot operates on a single channel, typically text, and responds to inputs by retrieving pre-programmed or retrieval-augmented answers. It does not take action. A multimodal AI agent is categorically different: it perceives and processes multiple types of input at the same time, including voice, text, images, and structured data, and then executes multi-step tasks autonomously using those combined inputs.

The difference becomes concrete in a lending scenario. A chatbot might answer the question "What documents do I need for a home loan?" A multimodal AI agent, given the same starting point, will conduct a voice conversation with the applicant, receive uploaded identity documents mid-call, verify them against live data sources, assess creditworthiness, and return a conditional pre-approval, all within the same interaction and without handing off to a human or an app.

This is not a speculative capability. Figure, a fintech offering home equity lines of credit, already uses Google's multimodal models to streamline lending experiences for both consumers and employees by combining voice, document, and transactional data in a single workflow.

Why BFSI Is the First Industry Where This Shift Is Already Happening

BFSI is not an accidental early mover. Three structural realities make it the natural proving ground for multimodal agents.

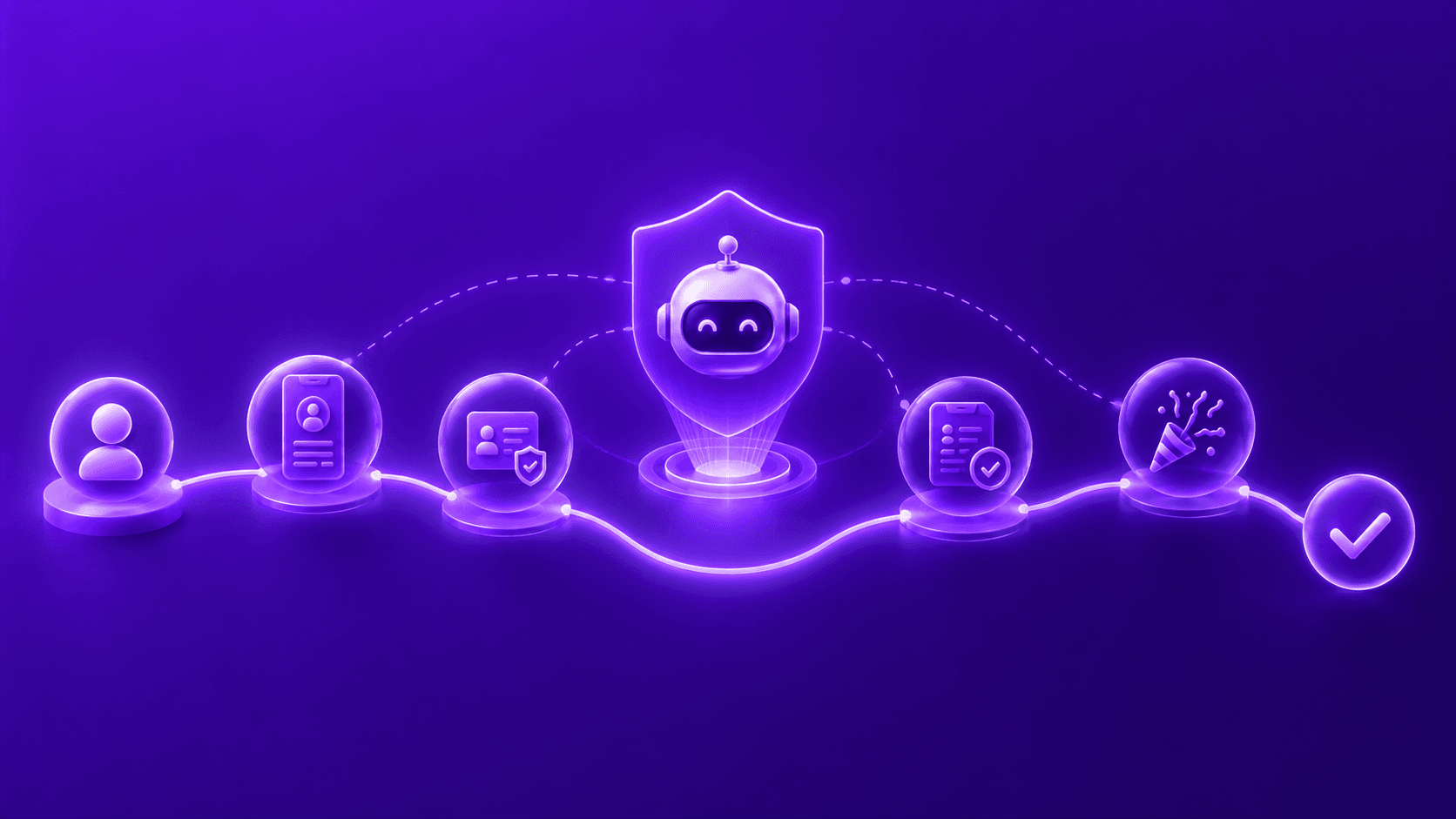

First, BFSI customer journeys are inherently multi-step and multi-modal. A KYC process requires identity documents, a live selfie or voice confirmation, and a data match against government or credit bureau records. A claims settlement requires a policyholder's account record, a voice description of the incident, and potentially a photo of damage. No other industry compresses this variety of data types into a single customer interaction as routinely as BFSI does.

Second, the cost of doing these interactions through human agents or app-based self-service is measurable and large. High-volume, repetitive interactions like EMI reminders, policy renewal prompts, and drop-off follow-ups are exactly where multimodal agents deliver disproportionate returns. Research published in 2026 indicates organizations achieve an average 2.3x return on agentic AI investments within 13 months, with banking and insurance sectors leading production deployments at 47% of enterprises.

Third, regulators have created explicit, auditable process requirements for identity verification, fraud screening, and compliance documentation. Multimodal agents, unlike human agents on ad hoc calls, can log every interaction modality and decision point, making compliance documentation a byproduct of the interaction rather than a separate step.

Mastercard has applied multimodal approaches to fraud prevention at the point of sale, layering transaction context with merchant graph data to identify suspicious patterns at scale. A challenger bank in the UK reduced onboarding time by 40% and reduced false positives in anti-money laundering checks by 30% after implementing multimodal verification workflows.

The Concrete BFSI Scenarios Where Agents Are Already Replacing App Screens

KYC via Voice and Document in One Call

Traditional KYC required a customer to download an app, navigate to a verification section, upload documents through a camera interface, wait for asynchronous review, and return later for the result. A multimodal agent compresses this into a phone call. The agent speaks with the customer, captures intent, guides document capture or receives a WhatsApp image mid-call, runs the verification against identity databases in real time, and confirms status before the call ends. The app screen is replaced by the conversation.

EMI Reminders That Actually Negotiate

A standard EMI reminder is a notification. An agentic EMI reminder is a conversation. The agent calls the borrower, identifies overdue status, presents restructuring options based on the borrower's profile and lender policy, accepts or counter-proposes payment arrangements, and updates the loan management system. No app screen is involved. No human agent is required for the majority of cases. The interaction is transactional and complete.

Policy Renewal Calls That Close

Insurance renewals have historically suffered from drop-off because the renewal journey required the customer to return to an app, review policy terms, and complete a payment flow. A multimodal renewal agent calls the policyholder, reads out key changes from the previous year's terms, answers questions in natural language, confirms coverage preferences by voice, and initiates the payment authorization, all in a single outbound call.

Drop-Off Reactivation

A customer who abandoned a loan application at the document upload stage is a recoverable lead. An agent can call that customer, identify exactly where the drop-off occurred by referencing the incomplete application, complete the remaining steps by voice or WhatsApp, and submit the application within the conversation. The app remains available, but the customer no longer needs it to complete the journey.

RevRag AI builds voice AI agents for BFSI institutions designed specifically for these scenarios: outbound calling, drop-off recovery, policy renewals, reactivation, and KYC. The architecture is built on the premise that the conversation is the interface.

What Replaces the App: Conversational Interfaces on WhatsApp and Phone

The mobile banking app is a navigation artifact. Its design is shaped by the assumption that a user needs to find their own way to a function, locate the right screen, and execute a task manually. That assumption breaks down when an AI agent already knows the customer's context, the pending action, and the optimal resolution path.

What replaces the app is not a new app. It is the conversation layer, delivered over existing channels the customer already uses: a phone call, a WhatsApp thread, or an SMS thread. The agent initiates, the customer responds, and the task completes. The interface is the voice or the message, not a screen the customer must locate and navigate.

This is already visible in intent-based navigation patterns emerging in enterprise software, where AI agents perform multi-step operations on behalf of users rather than presenting menus for the user to navigate. In BFSI, the implication is direct: balance checks, EMI payments, KYC submissions, policy renewals, and loan applications can all resolve conversationally on channels with near-universal penetration, while the app becomes a reference tool for edge cases rather than the primary interaction surface.

Timeline: Why Sooner Than Most Expect

The conventional technology adoption curve suggests years of gradual penetration before incumbent patterns change. Multimodal agents in BFSI are running on a compressed timeline for two reasons.

The first is the channel infrastructure is already in place. WhatsApp has over two billion active users globally. Phone networks reach every borrower, policyholder, and account holder a BFSI institution serves. There is no new channel to build or adopt. The agent deploys on infrastructure the customer already uses daily.

The second is that enterprise adoption has already crossed the threshold of proof. Research from 2026 places 44% of finance teams using agentic AI, representing a growth rate exceeding 600% from the previous year. Applications embedding agent capabilities are projected to grow from under 5% in 2025 to 40% in 2026. The market for AI agents in financial services is valued at $1.96 billion in 2026 and is projected to reach $5.71 billion by 2034.

Separately, 70% of banking executives describe agentic AI as having a "significant" or "game changer" impact on the future of banking, according to 2026 industry research. When the majority of decision-makers in a capital-intensive, risk-aware industry share that view, deployment timelines accelerate.

What This Means for BFSI Institutions Building for the Next Three Years

Institutions that treat multimodal agents as a future consideration rather than a current infrastructure decision will find themselves in a reactive position. The BFSI institutions that are ahead are not experimenting at the margins. They are rebuilding customer journey logic around the assumption that the conversation is the primary interface and the app is secondary.

Three specific planning implications follow from this.

Channel strategy should be reoriented around conversational completion rates, not app engagement metrics. If an EMI collection journey can close on a voice call without requiring the borrower to open an app, the success metric changes from app session length to conversation resolution rate.

Data architecture must accommodate multimodal inputs. Voice transcripts, document images, and structured transaction data need to flow into the same agent context so the agent can reason across all of them. Institutions with siloed voice, document, and core banking systems will find multimodal agents difficult to deploy effectively until those silos are bridged.

Vendor selection should prioritize BFSI-specific deployment experience over general-purpose AI capability. The compliance requirements, conversation design constraints, and integration patterns in BFSI are distinct from those in retail or logistics. Agents built for BFSI workflows are operationally closer to production than general-purpose agents adapted post hoc.

The core bet is straightforward: the customer does not want to navigate an app to accomplish something a voice call can resolve in two minutes. As multimodal agents close the gap between what a conversation can accomplish and what an app can accomplish, the case for the app as a primary channel narrows. In BFSI, where the gap is already closing fast, this is a planning horizon measured in months, not years.

FAQ

What is a multimodal AI agent in banking?

A multimodal AI agent in banking is an AI system that can simultaneously process and act on multiple types of input, including voice, text, images, and structured financial data. Unlike a simple chatbot that responds to typed queries, a multimodal agent can conduct a phone call, receive uploaded documents during that call, verify identity against external databases, and complete a transaction, all within a single interaction. These agents are deployed across KYC, loan origination, fraud detection, and customer service workflows in BFSI institutions.

How is a multimodal AI agent different from a traditional banking chatbot?

A traditional banking chatbot is a single-channel, response-only tool. It reads text input and returns text output, typically drawing on a fixed knowledge base or FAQ. A multimodal AI agent operates across voice, text, and document channels simultaneously, takes actions on backend systems, and completes multi-step workflows autonomously. The chatbot answers the question; the multimodal agent resolves the underlying task.

Which BFSI use cases are most suited for multimodal AI agents?

KYC verification, loan drop-off recovery, EMI collection and restructuring, insurance policy renewals, and fraud screening are the highest-priority use cases in current BFSI deployments. These workflows require combining voice interaction, document verification, and real-time data lookup, exactly the capabilities that multimodal agents are designed to handle. Organizations in banking and insurance are leading enterprise AI agent adoption at 47% of companies with at least one agent in production, according to 2026 research.

Will multimodal AI agents completely replace mobile banking apps?

The more accurate framing is that multimodal agents will absorb the majority of transactional use cases that currently require apps, leaving apps as reference tools rather than primary interaction surfaces. For complex advisory functions, document archives, or preference management, apps retain utility. For payments, identity verification, EMI negotiations, and renewal completions, conversational agents on phone and WhatsApp channels can resolve the journey without an app. The shift is gradual but directionally clear.

What channels do multimodal AI agents use to reach banking customers?

Multimodal AI agents in BFSI currently operate primarily over phone calls and WhatsApp, with SMS as a secondary trigger channel. These channels reach the full customer base of a BFSI institution without requiring any app installation or login. Voice calls handle the conversation and negotiation layer; WhatsApp handles document receipt and asynchronous follow-up. The agent orchestrates both within the same customer journey.

How long does it take for a BFSI institution to see ROI from agentic AI?

Research published in 2026 indicates that organizations achieve an average 2.3x return on agentic AI investments within 13 months. In BFSI specifically, credit unions report strong returns across automated compliance and customer support use cases. ROI timelines of 6 to 12 months are commonly cited for high-volume use cases like EMI reminders, renewal calls, and KYC automation where the cost per interaction is clearly measurable.

See RevRag in action

Book a demo and see how agentic AI can transform your BFSI customer journeys.

Book a Demo